This article is a repost. It was originally published by The Solari Report

The U.S. Federal Reserve and its central banking allies are engineering unprecedented changes in the financial system. How do we know this? Because they speak openly about what they intend to do.

I want to show you three 1-minute videos today that describe the vision of total central control currently being implemented by the central banks.

The first is a clip from an IMF panel in October 2020. The speaker is Agustín Carstens, the general manager of the Bank for International Settlements (BIS) in Basel, Switzerland. The BIS is the central bank of central banks, which enjoys the powers of sovereign immunity. The Federal Reserve is one of 63 central banks which are BIS members, including the Bank of England, the European Central Bank, and the Bank of China.

In this clip, Mr. Carstens is describing the nature of central bank digital currency or CBDC. The BIS is leading a global effort to implement CBDC, including a partnership with the Federal Reserve.

Let’s see what Mr. Carstens says about where he hopes our money is going.

Agustín Carstens, BIS General Manager: Central Banks Will Have Absolute Control

So, what did he just say?

He just said that our bank deposits are not ours—our bank deposits are an “expression of central bank liabilities”—in other words, it is their money, not ours.

He said that the central bankers will have complete surveillance and control of when, where, and how we can use our bank deposits.

And he said that they can enforce the rules centrally.

In short, our banking system is being transformed from a financial system to a control grid. Mr. Carstens believes that he can put us in digital financial concentration camps and make and enforce the tyrannical rules from outside your state.

He believes that central bankers should be able to control who and how the people of your state can do business and with whom we can trade, including in your state.

The second video I want you to see is Bo Li, the former Deputy Governor of the Bank of China, now the Deputy Managing Director of the International Monetary Fund (IMF), explaining the ability that this technology gives the central banks and governments to program money.

What does this mean? If the rules say you cannot travel more than 15 miles from your home, your money will not work more than 15 miles from your home. If the rules say you cannot eat pizza, your money will not work when you try to buy pizza. Want to disarm the people in your state? Just turn off the bank accounts and credit cards of anyone who refuses to turn in their guns. Shut down the bank accounts of gun stores and dealers. Make sure no one’s money can pay for ammunition. If a State senator or House representative or candidate objects, just freeze their bank accounts, too. While you are at it, turn off their phone and Internet access. Turn off their electricity and gas.

Bo Li, Deputy Managing Director at the IMF: On the Programmability of Digital Money

Lest you think this is an exaggeration of how tyrannical this vision is, let’s look at the third video.

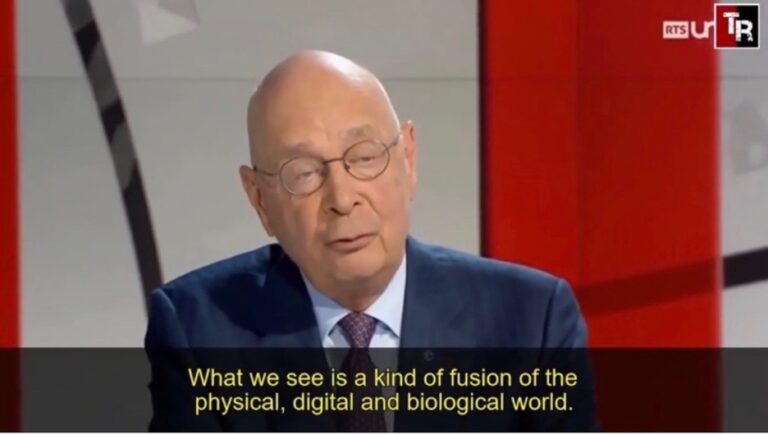

This is a presentation by Neel Kashkari, President of the Minneapolis Federal Reserve Bank—one of the 12 privately owned Federal Reserve Banks that make up the U.S. federal reserve system along with the Federal Reserve Board of Governors in Washington. Mr. Kashkari was speaking earlier last year at Columbia University and this is what he had to say about the plans to launch a central bank digital currency.

Neel Kashkari, President of the Minneapolis Federal Reserve: Why Would the American People Be for [CBDC]?

So, the plans for central bank digital control and numerous other digital financial mechanisms to control your communications and transactions are so bad that the central bankers themselves are afraid for our country and warning us that we do not want to do this.

I want you to see these videos because it is important to understand the push for total control through the weaponization of the financial system. We see the Canadian truckers and those who support them have their bank accounts frozen. We see politicians in the UK thrown out of banks. We see companies telling us the truth about how to stay healthy thrown out of big banks. If we do not act to stop this, these things will happen to people and businesses in your state.

How are you going to protect the financial transaction freedom of your state and its banks, businesses, and residents? This is the question before us—and it is your responsibility and yours to answer and address.

Related:

For a wealth of information about what you and your state legislators and officials can do—and what they are doing around the country—check out our site to support the push to protect financial transaction freedom.